Esteban Duverge

Esteban DuvergeCOVID-19 might have accelerated the adoption of digital channels in the banking industry, but customers’ reliance on digital channels over physical ones will outlive the pandemic.

The impact of COVID-19 made customers seek refuge in digital channels, accelerating the pace of digital adoption. With consumers relying more on online services and their smartphones, traditional and challenger banks with robust digital capabilities benefited from the uptick in digital activity.

Long Lasting Effects

Fear of being exposed to COVID-19 made customers shelter themselves in digital channels to interact with their FSIs. After the pandemic, certain behaviors will go back to normal, but according to the Mintel Global Trend Driver Technology “consumers will rely more heavily on their devices to interact with their FSIs.” Now that consumers tasted the convenience of mobile banking, it will be difficult for them to go back to interacting with their FSIs in a more traditional way – for example, by visiting a branch.

The consumer exodus to digital channels benefited both traditional and challenger banks that entered the pandemic with robust digital capabilities. According to FIS, JD Power, there was a 200% increase in mobile bank registrations in April 2020 versus March 2020, and an 85% increase in mobile traffic in the same time period.

Digital Sees Uptick

With Revolut entering the U.S. market, Varo becoming the first mobile bank to be granted a national bank charter, and Chime becoming the most valuable American fintech startup, it is clear that the accelerated adoption of digital channels spurred by COVID-19 benefited both online and mobile banks. These challenger banks are becoming more prominent in the banking landscape, posing real competition for traditional banks in the short and long term.

However, Given its mobile-only nature, mobile banks did not promote their apps in the same way as traditional or even online banks did. The value proposition of N26 and Revolut is entirely tied to the performance of their mobile app, which is why they don’t promote their apps as a separate entity from their accounts, but as improved accounts enabled by technology.

N26 focuses on delivering a fast, flexible, and transparent banking experience through technology.

Credit: Comperemedia Direct

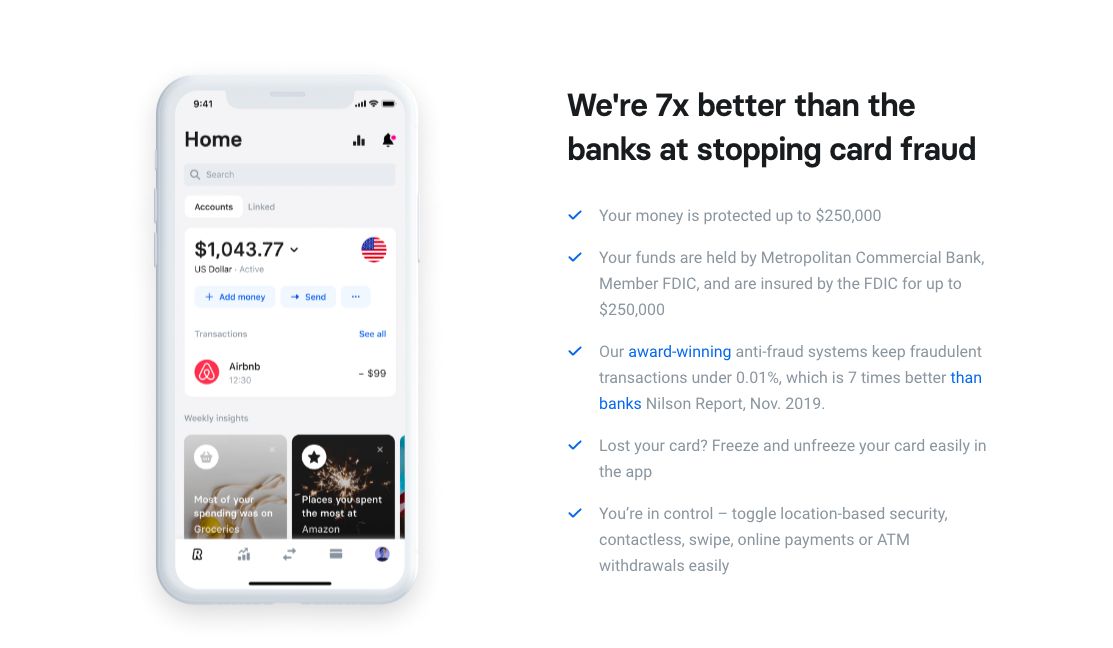

Revolut not only promoted common features found in mobile apps from traditional banks, it also stated that its anti-fraud system is “7 times better than banks,” positioning itself as a better alternative than traditional banks.

Credit: Comperemedia Direct

Emails often highlighted two important factors that make the case for mobile apps: convenience and control.

Bank of America highlighted the number of users that utilize the app and encouraged the reader to “get your banking done easily and securely,” while Citibank explained that, with its mobile app, customers had the same capabilities as if they were visiting a branch or calling customer service. Chase motivated customers to enhance their access by using its app.

Chime leveraged Nerdwallet’s recognition of its app to position it as a trustworthy and efficient tool.

Emails from both traditional and challenger banks highlighted mobile deposits as an advantage of their mobile apps – a much needed feature amid the pandemic.

Bank of America utilized a simple four-step guide to demonstrate how easy it is to deposit a check through the mobile app.

Credit: Comperemedia Direct

Just like Bank of America, Ally also utilized a step-by-step guide to showcase how easy it was to deposit a check trough the mobile app.

Citibank talked about how easy it was to deposit checks right at home – even stimulus checks and Wells Fargo highlighted that customers were able to deposit a check on their own schedule while skipping the trip to a branch.

Chime stated that in order to enjoy mobile check deposit, account holders needed to sigh up for direct deposits first.

Other features that were highlighted in emails were digital assistants and the convenience of Zelle.

Checking and Savings Remain on Top

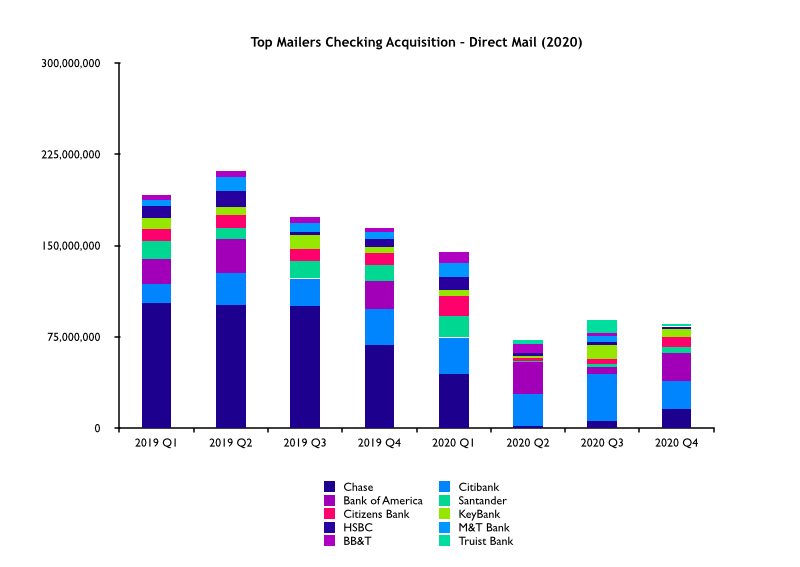

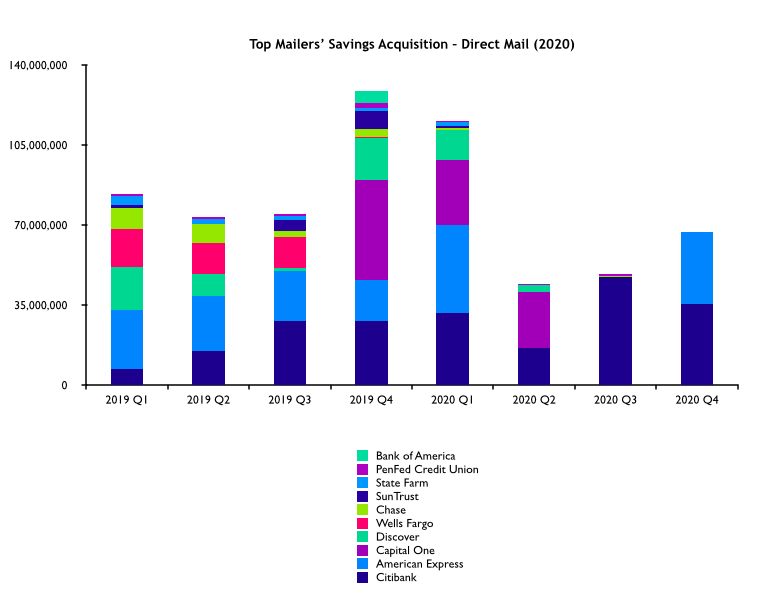

Checking and savings remained the preferred product lines on which banks relied on to drive new business. Overall deposit acquisition offers in direct mail saw a YoY volume decrease of 69% in Q2 2020. Citibank, which was the top mailer for both checking and savings in 2020, leveraged its existing customers to drive new business.

Email echoed direct mail, with checking and savings leading all banking offers. Due to email’s inherent cross-sell nature, banks used it to drive new business among current customers.

Checking

Citibank surpassed Chase as the top mailer in 2020, focusing on driving new business by leveraging the relationship with its existing customers.

Click to enlarge. | Credit: Comperemedia Direct

Despite the pandemic, average incentives increased significantly, signaling that banks were willing to pay more for new checking customers. Top mailers crafted their top campaigns’ acquisition messaging around their cash bonuses, positioning the dollar amount at the top of their communications.

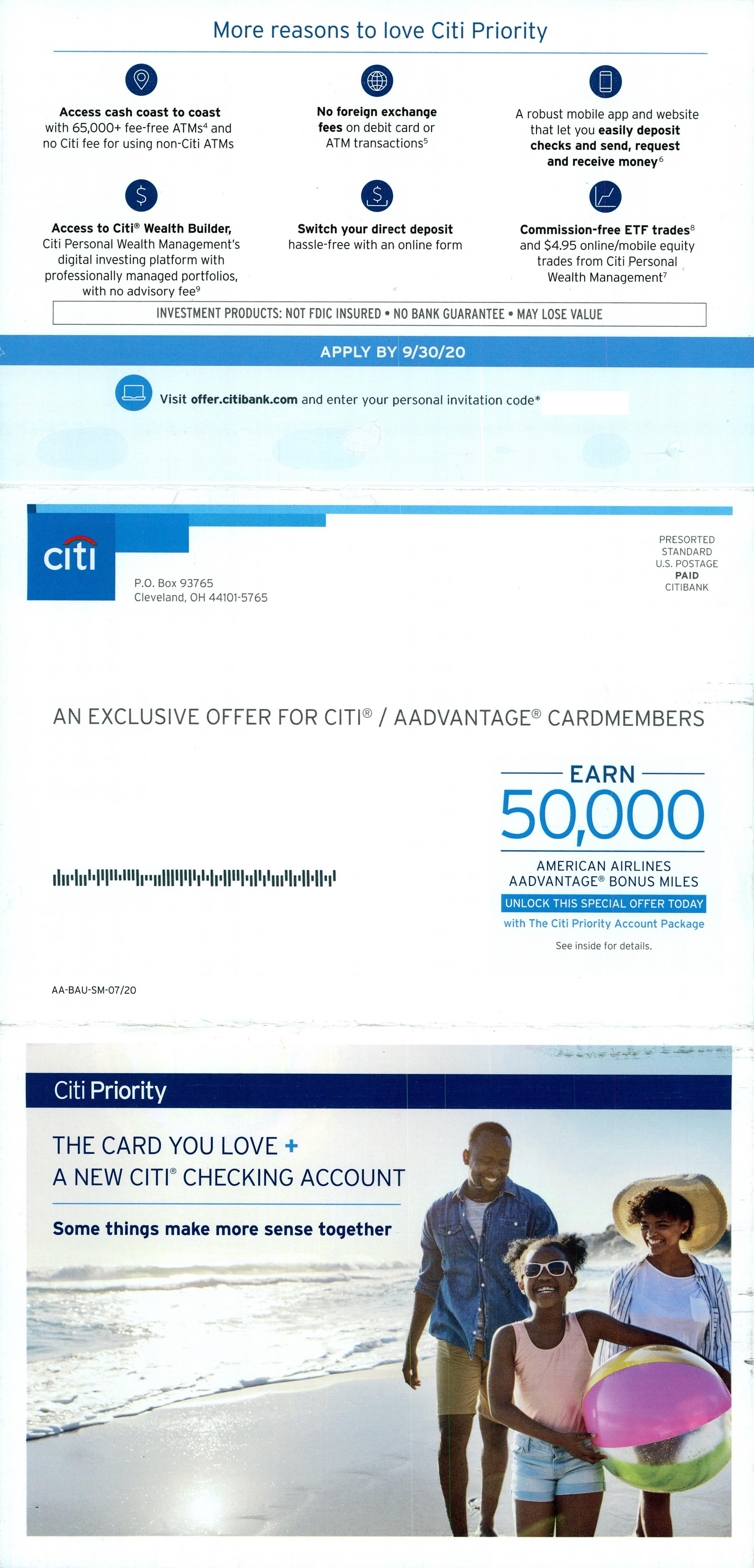

Citibank opted for a tiered offer ranging from $200 to $1,500, giving customers the opportunity to earn more based on their minimum deposit.

Credit: Comperemedia Direct

Citibank was the only top mailer that featured bonus points and miles as a checking incentive in 2020.

Credit: Comperemedia Direct

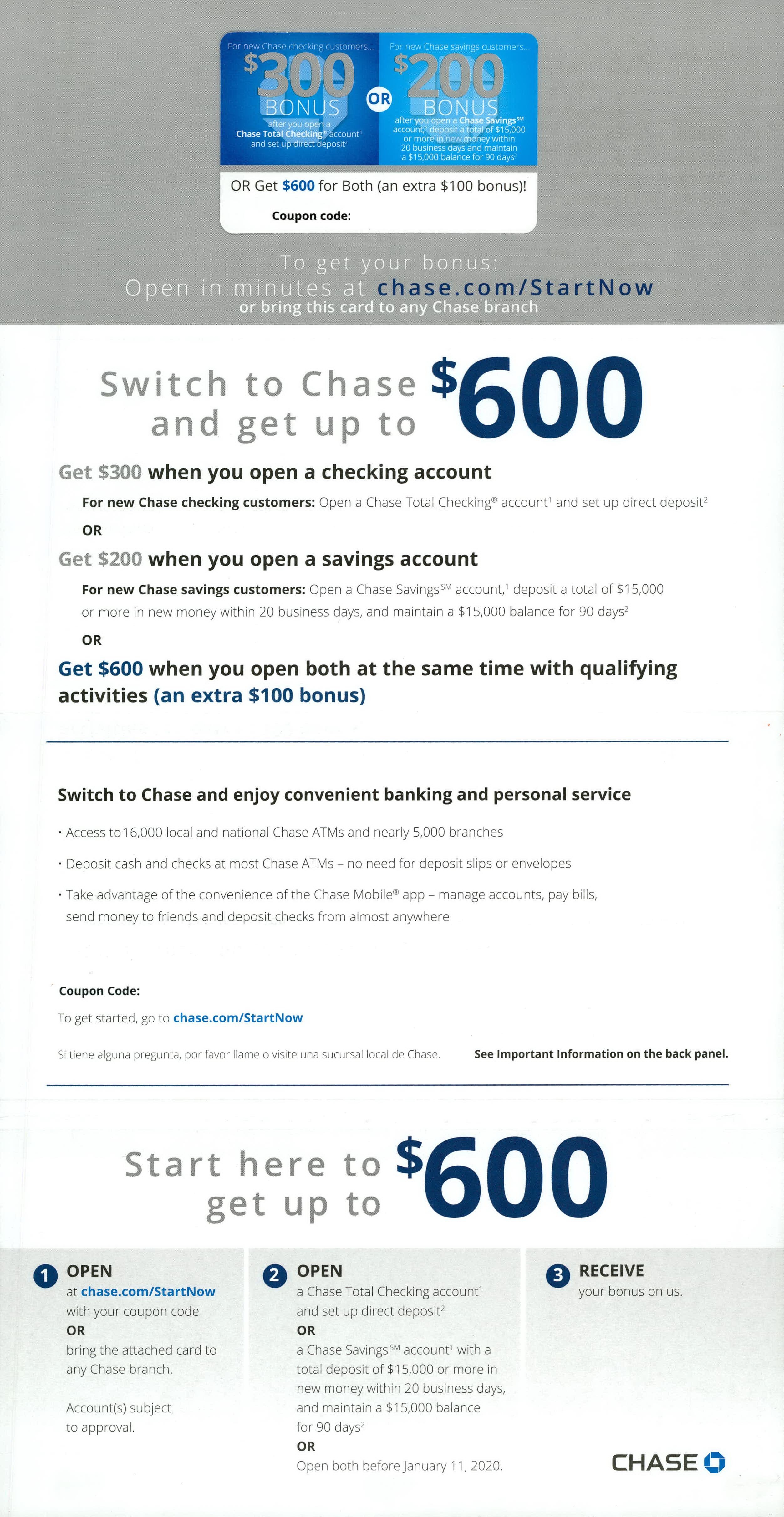

Chase offered up to $600 for customers who open a checking and savings account.

Credit: Comperemedia Direct

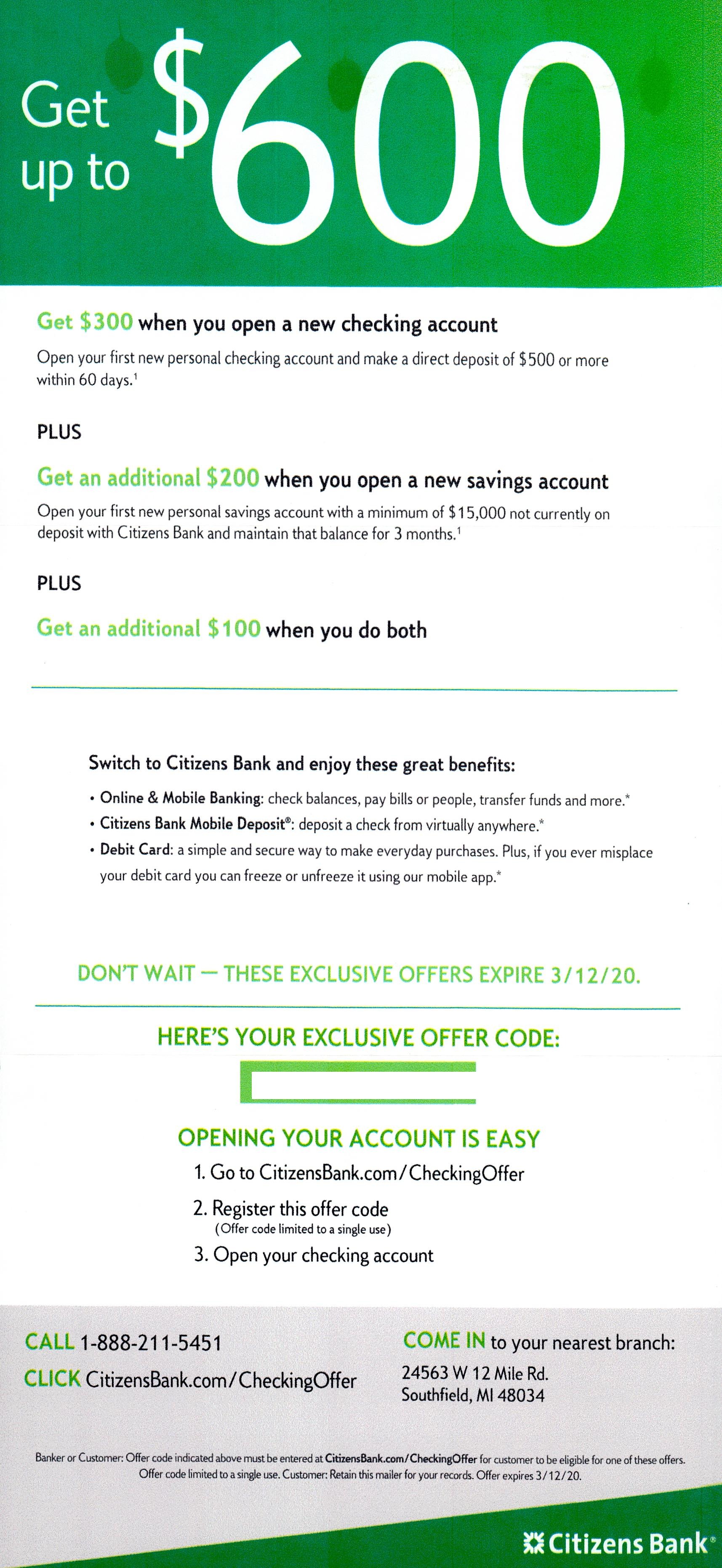

Just like Chase, Citizens Bank offered up to $600 to customers who open a checking and savings account.

Credit: Comperemedia Direct

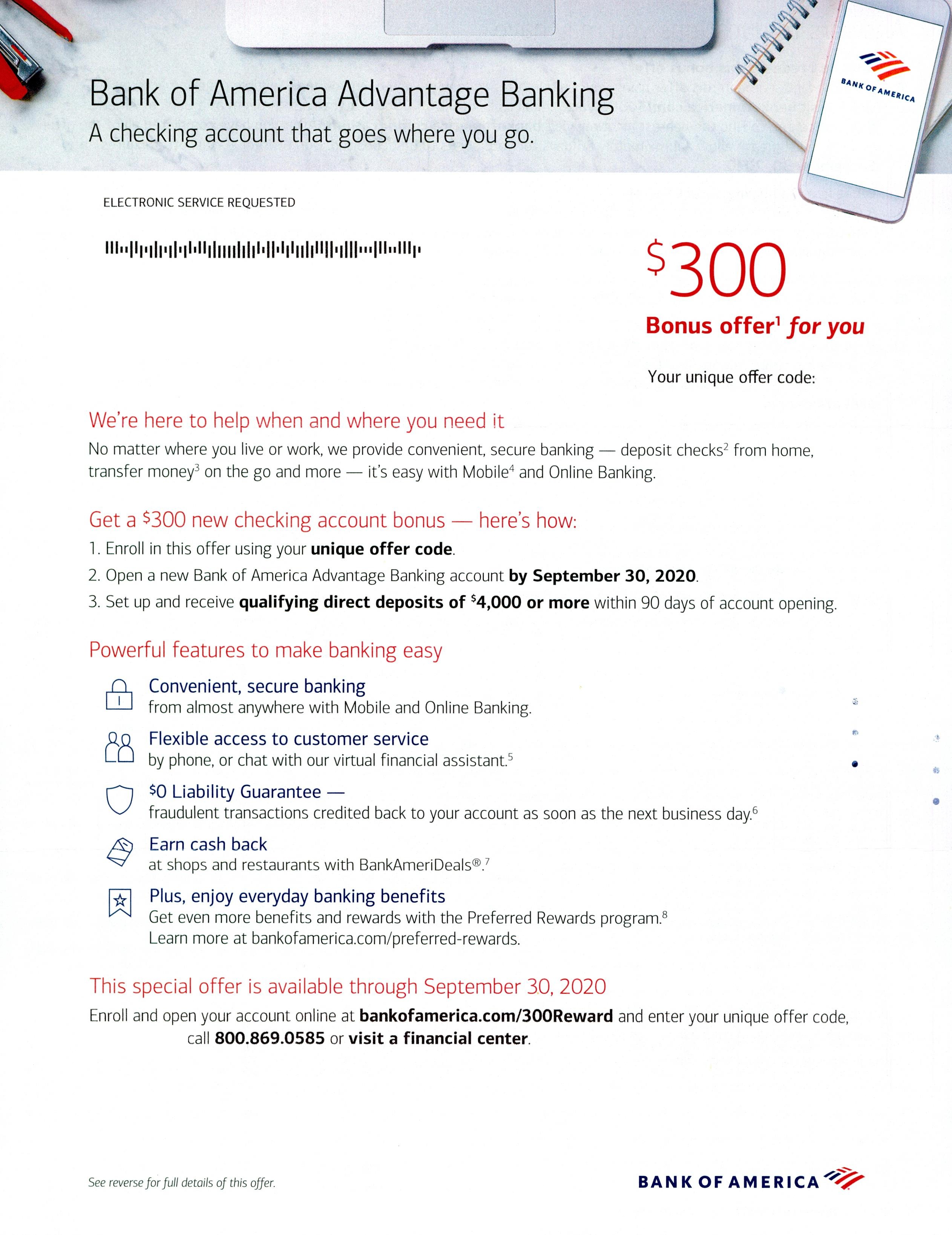

Bank of America featured a $300 bonus after receiving direct deposits of $4,000.

Credit: Comperemedia Direct

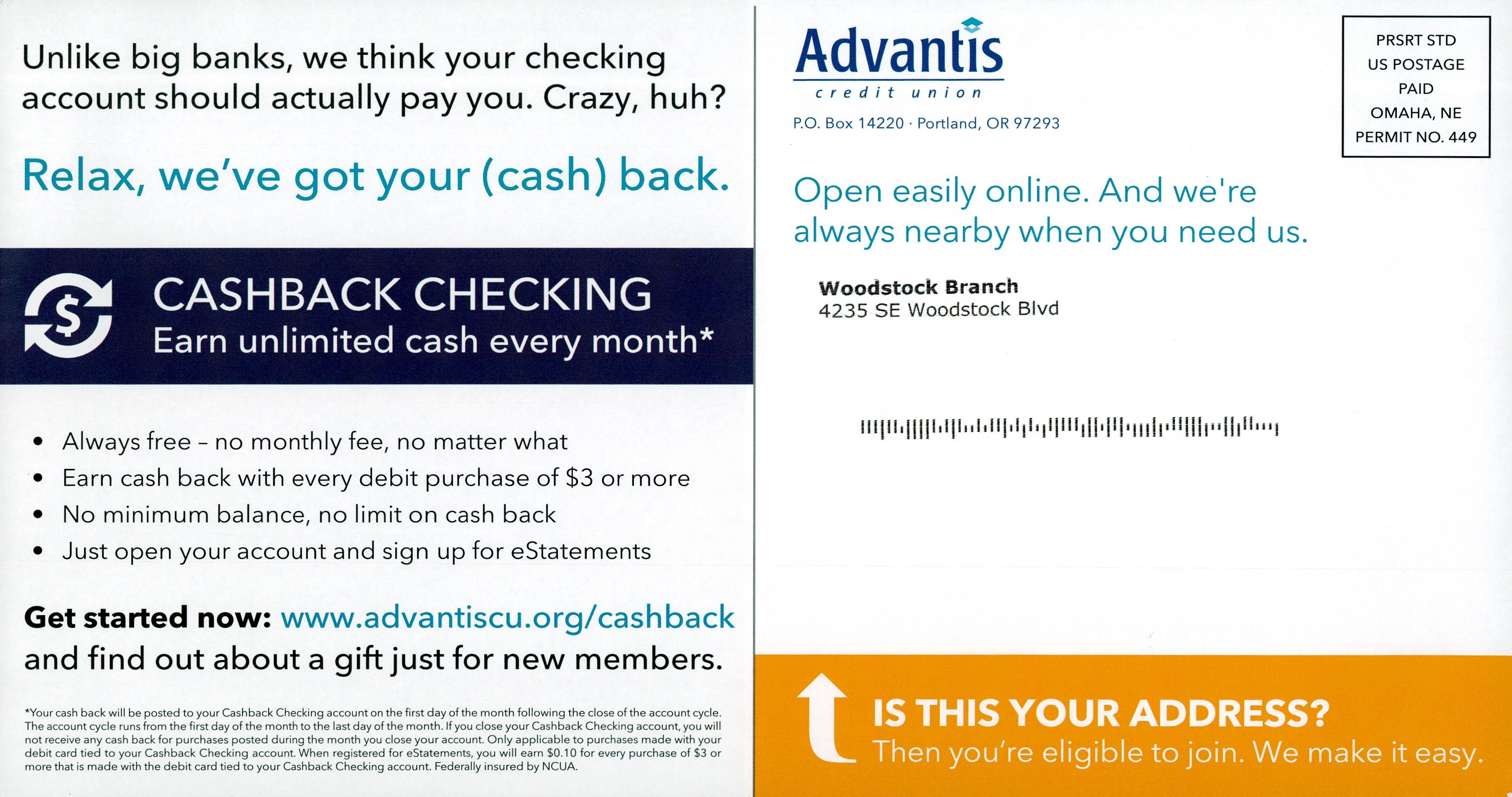

Smaller banks and credit unions highlighted the lack of fees in their checking accounts, motivating customers to stop banking with “big banks.”

Advantis Credit Union stated that its Cashback Checking account would “earn unlimited cash every month,” unlike the checking accounts from big banks.

Credit: Comperemedia Direct

Banner Bank’s value proposition revolved around not having “monthly service fees and no hidden catches,” stating that big banks “always seem to get you with some catch – like a minimum balance requirement.”

Credit: Comperemedia Direct

American Eagle Financial Credit Union summarized its value proposition in two sentences: “Hassle-free checking. No big bank fees.”

Credit: Comperemedia Direct

Online banks such as Simple and Chime relied on the word “free” to promote the features of their checking accounts. Simple promoted $0 monthly maintenance fee on its Protected Goals account as a way to “bank like a boss.” Chime did not only promoted its fee-free overdraft feature “SpotMe,” it also included Nerdwallet’s recognition to boost its credibility among consumers.

Savings

Citibank surpassed Capital One as the top mailer in 2020. Just as with its checking products, Citibank relied entirely on existing customers to drive new business. Capital One promoted its 360 Performance Savings account aggressively from Q4 2019 to Q2 2020. For the remainder of 2020, Capital One shifted its focus to its 360 Checking account, halting all promotions on its savings account. This strategy shift allowed Capital One to fall behind Citibank.

Click to enlarge. | Credit: Comperemedia Direct

Savings offers with incentives have been declining steadily since the beginning of 2020, reaching their lowest point at the end of the year. The decline in savings offers with incentives can be attributed to Capital One and Discover, which sent 39.2 million and 16 million of offers in Q4 2019, respectively, and none in Q4 2020. Citibank was the only top mailer that increased its savings offers with incentives, going from 371,000 in Q4 2019 to 6.2 million in Q2 2020.

With interest rates close to 0%, big banks and credit unions stopped disclosing their APYs later in 2020, relying only on the national average to benchmark their rates.

Q3 2020 | Credit: Comperemedia Direct

Online banks promoted their tools as a way to help account holders automate budgeting and saving.

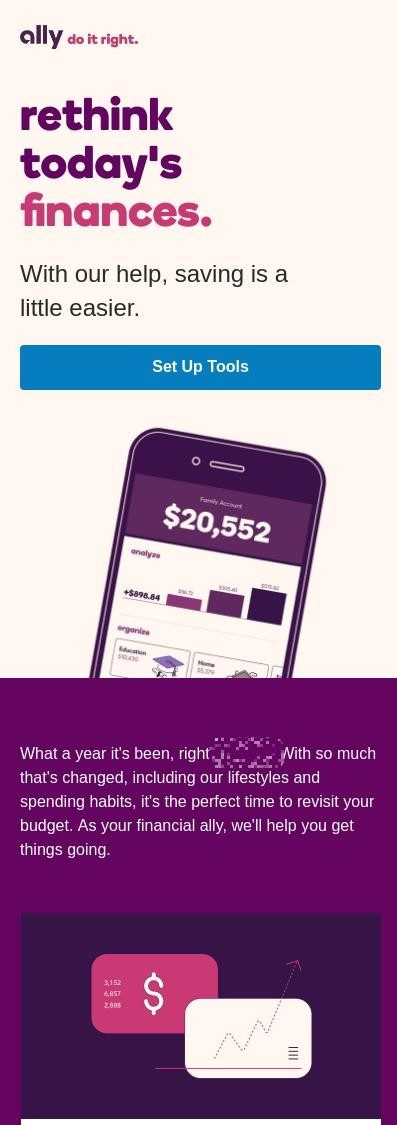

With the subject line “a new lifestyle for a new budget,” Ally Bank addressed the impact of COVID-19 on our financial lives. The online bank promoted its set of tools to help customers reach their goals, claiming that “smart saving begins here.”

Credit: Comperemedia Direct

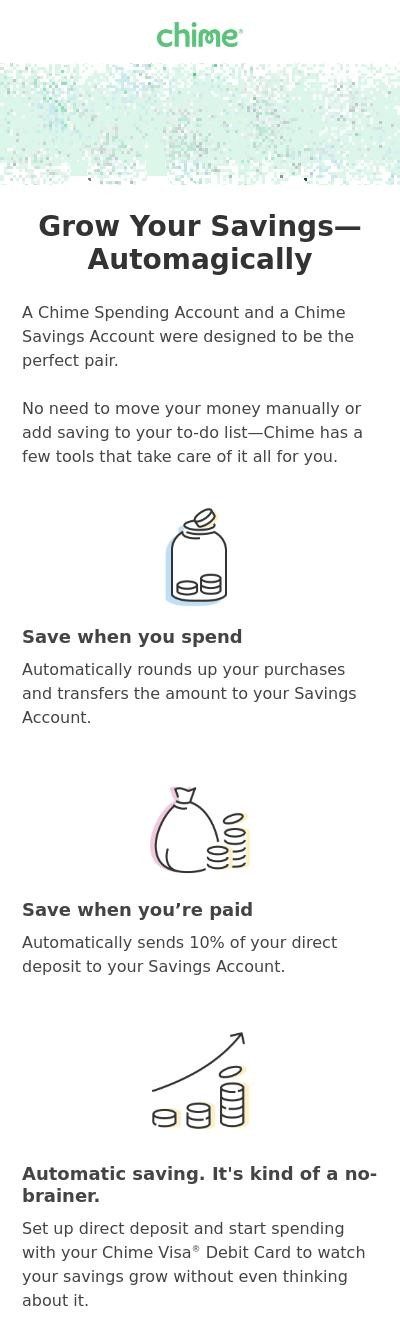

Chime promoted its tools as a way to automate savings with “no need to move your money or add savings to your to-do list.”

Credit: Comperemedia Direct

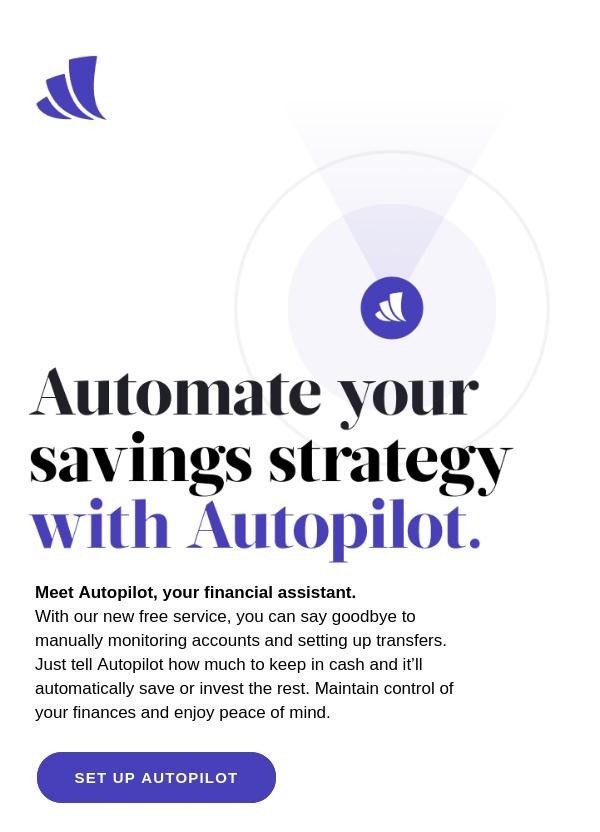

Wealthfront promoted its Autopilot feature, as a way to help account holders to automatically save or invest.

Credit: Comperemedia Direct

Certificates of Deposit

Only four out of the top 10 mailers kept promoting their certificate of deposits after Q1 2020, reflecting the impact the pandemic had on the product line. Certificate of deposit offers among top mailers fell 69% from 2019 to 2020. Discover, which saw its volume decrease by 39%, was the main driver for the overall decline in the product line.

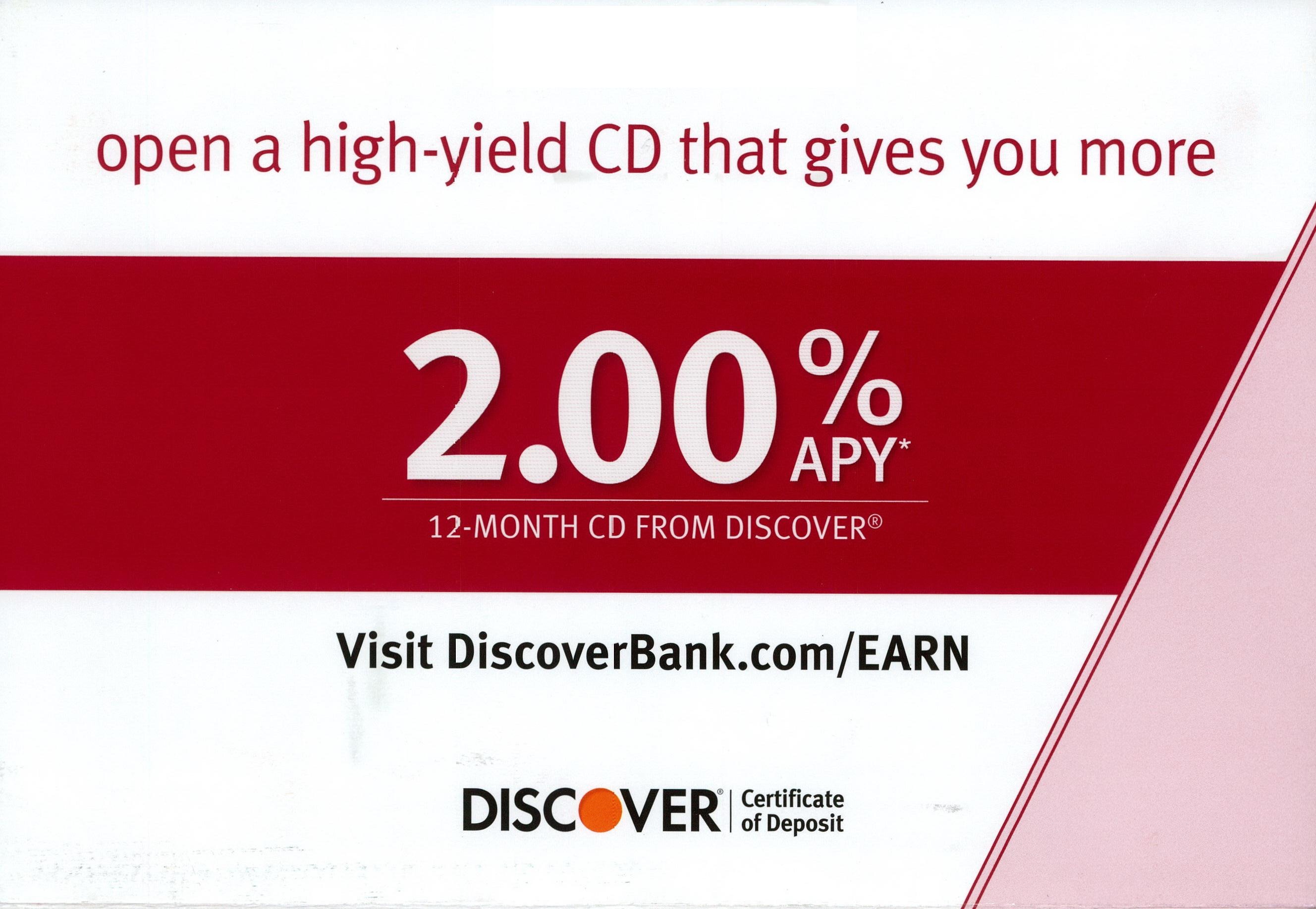

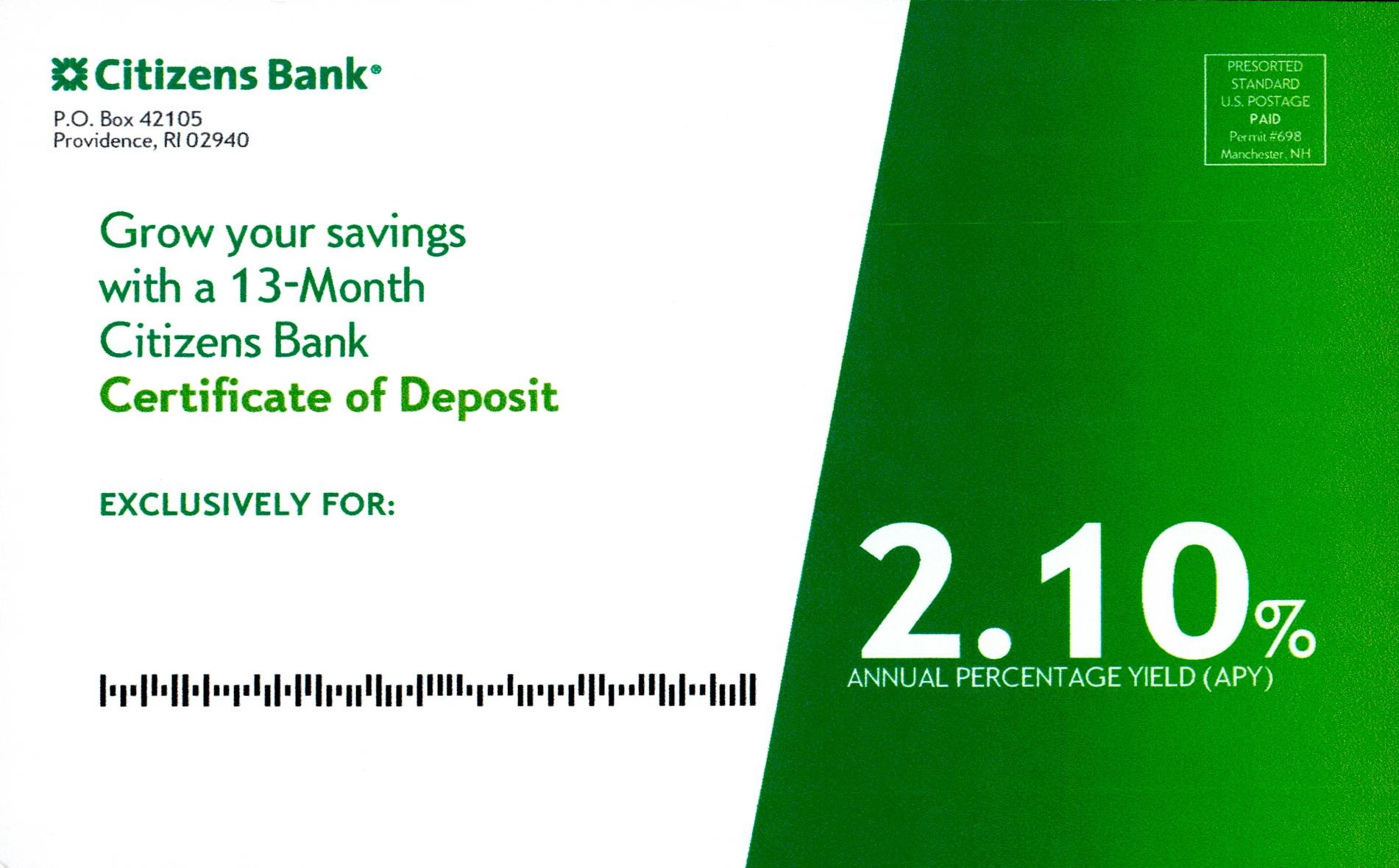

Top campaigns positioned certificates of deposit as the smart way to put money to work. Both Discover and Citizens Bank made their APYs front and center of their communications. Discover highlighted how easy it was to open a CD by providing a 3-step guide, while Citizens Bank motivated customers to call or visit a branch to open a CD.

Credit: Comperemedia Direct

Credit: Comperemedia Direct

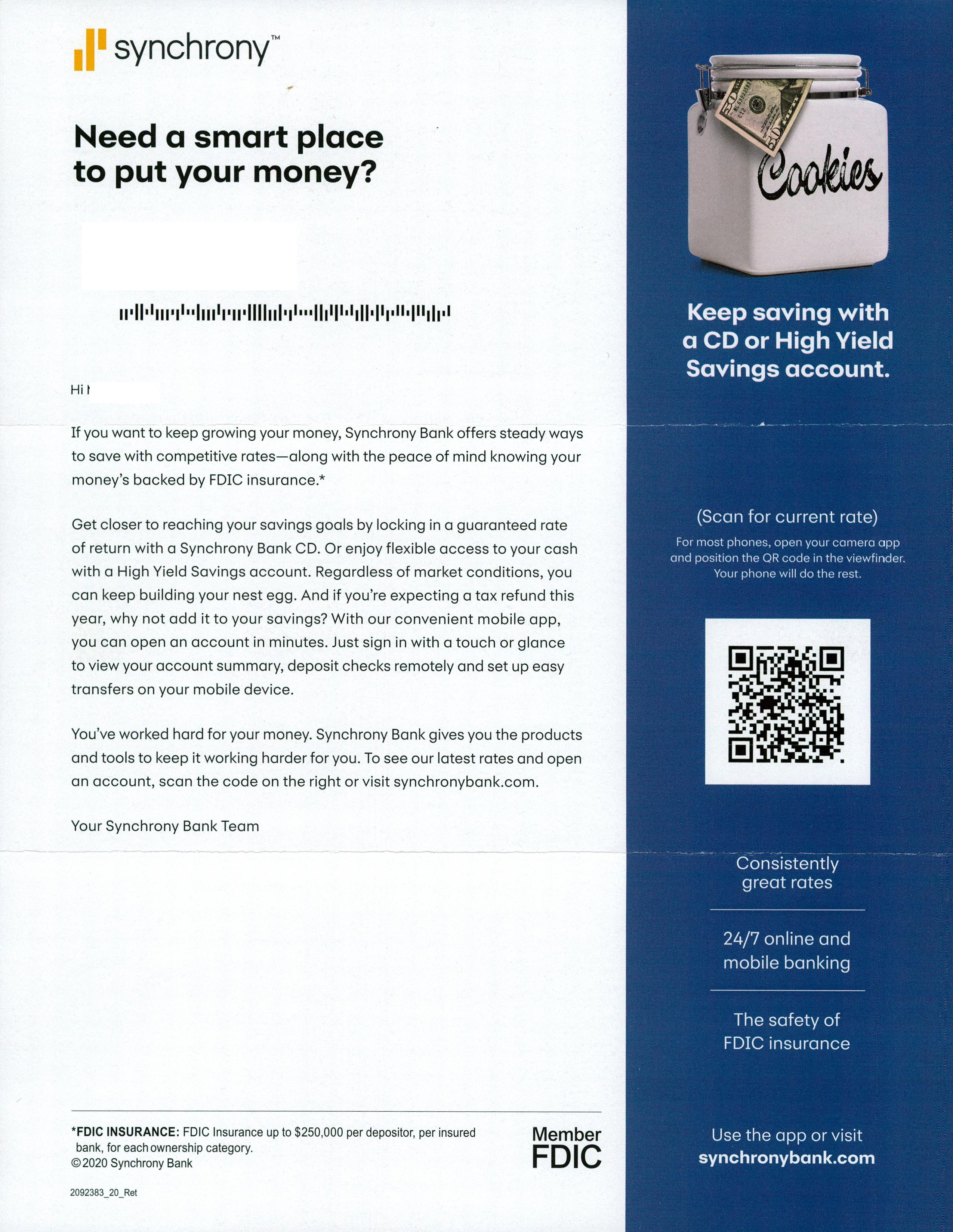

With rates plummeting amid the pandemic, Synchrony Bank included a QR code so that customers could take a look at the latest rate.

Credit: Comperemedia Direct

Money Market Accounts

Top mailers stopped promoting money market accounts after Q1 2020. This was driven by Capital One, which stopped sending money market offers after Q3 2019.

Huntington Bank had the top campaign of 2020, where it promoted its Relationship Money Market account. The bank relied on its J.D. Power award to give its product more credibility among consumers.

Credit: Comperemedia Direct

Debit Cards

Debit card communications fell 43% from 2019 to 2020. Top mailer Capital One drove this decline, dropping its debit card communications by 43% in 2020. The vast majority of Capital One communications were observed in the last quarter of both 2019 and 2020, signaling the bank’s seasonality when it came to debit cards. However, Capital One’s volume drop in 2020 made it possible for Navy Federal Credit Union to become the top mailer of the year.

Navy Federal highlighted the security aspect of the card through its “Zero Liability” policy, citing features such as 24/7 fraud prevention system, encryption technology, and more.

Credit: Comperemedia Direct

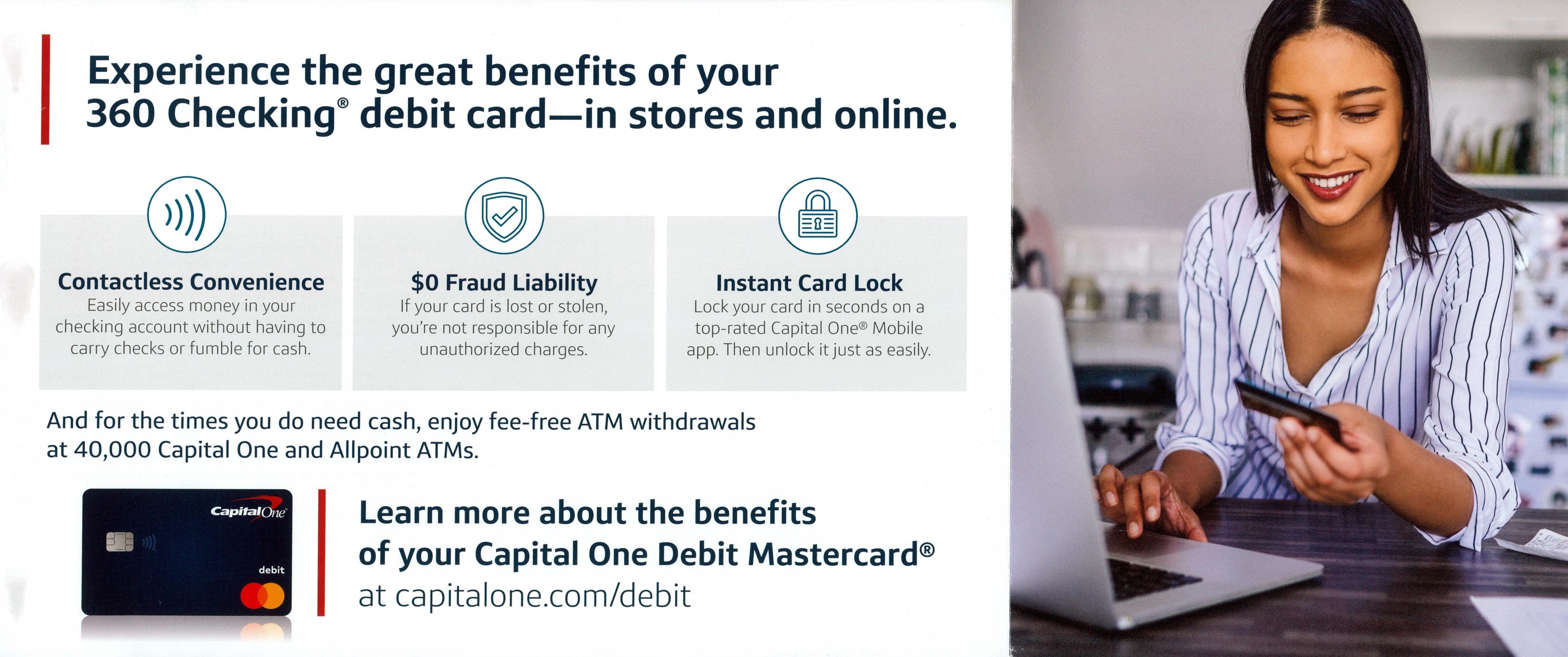

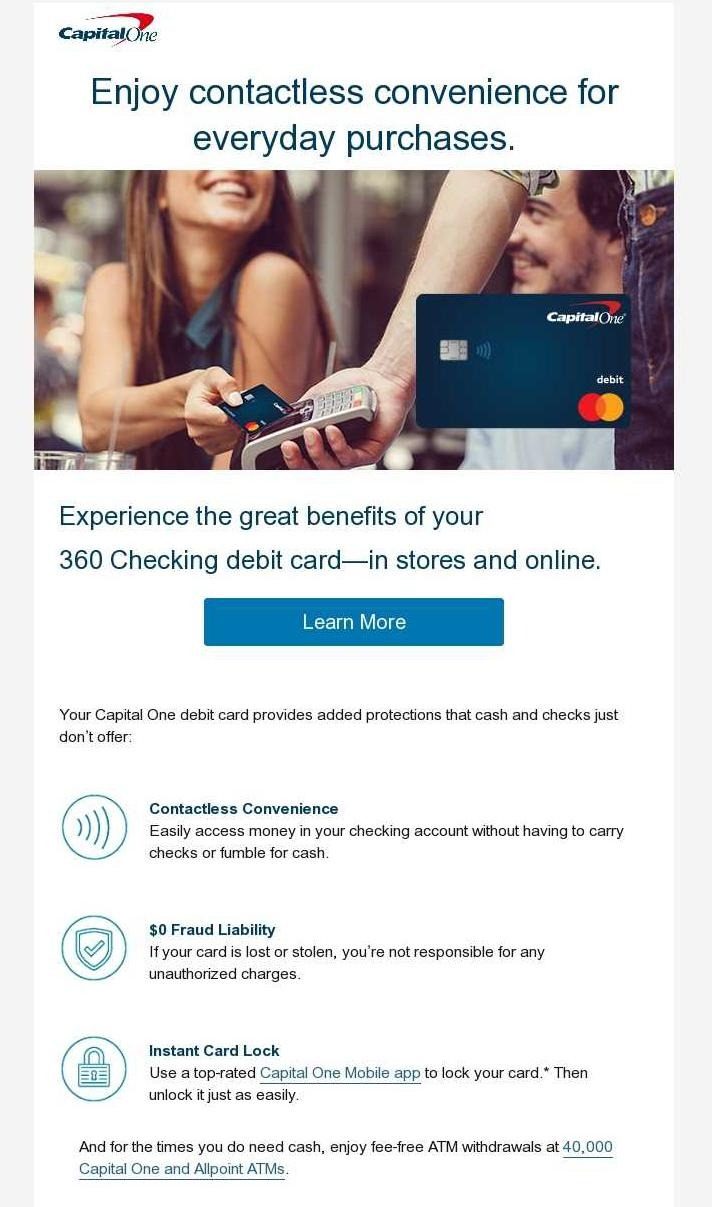

In addition to its $0 fraud Liability and Instant Card Lock, Capital One led the value proposition of its debit card with its contactless convenience, a welcome feature amid the pandemic

Credit: Comperemedia Direct

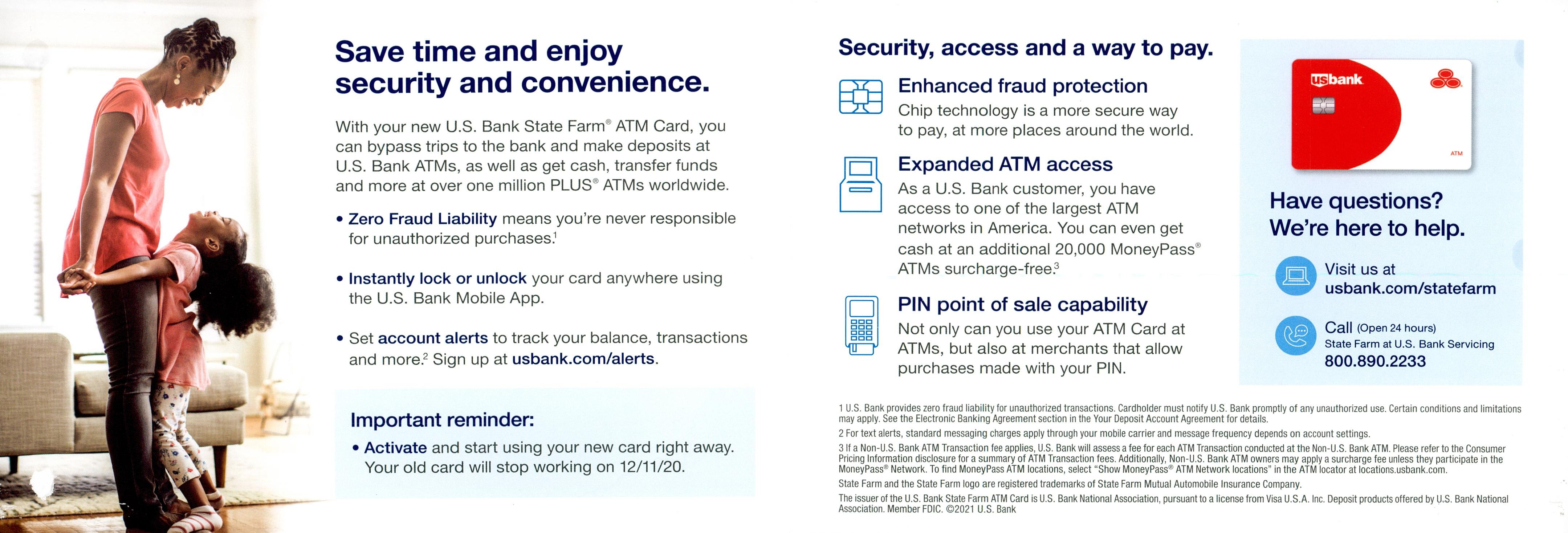

U.S. Bank highlighted its chip technology for an enhanced fraud protection and its expanded ATM access.

Credit: Comperemedia Direct

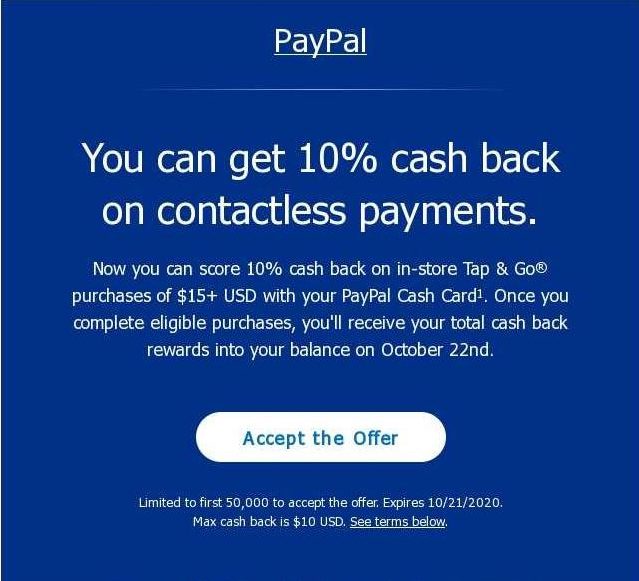

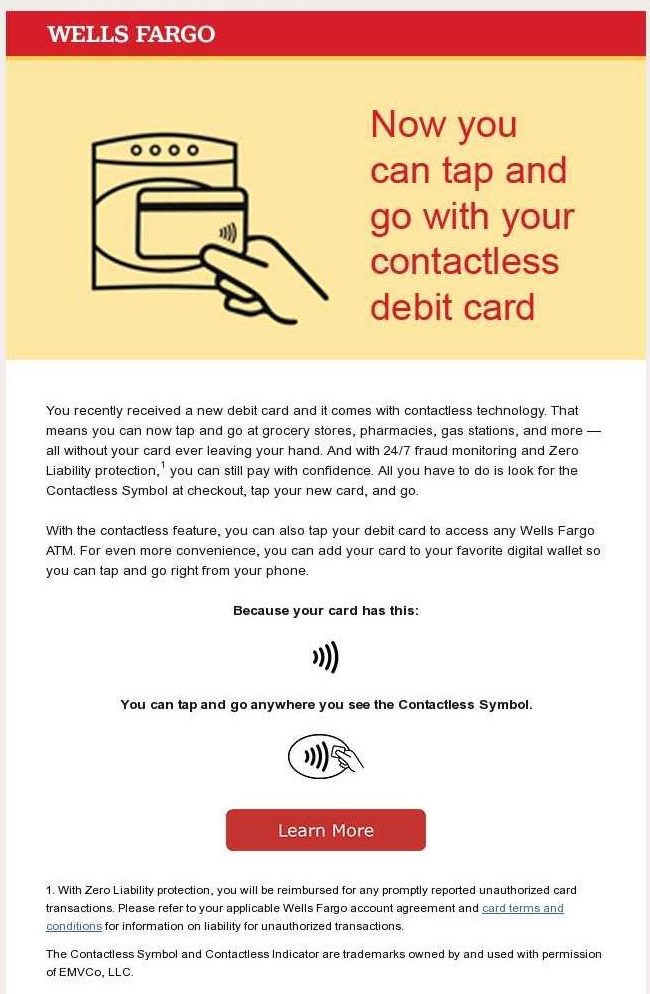

Some banks promoting the contactless capabilities of their debit cards missed the opportunity to position the feature as the safest way to pay amid the pandemic.

PayPal rewarded cardholders who used the card’s Tap & Go feature with a 10% cash back.

Credit: Comperemedia Direct

Wells Fargo motivated cardholders to use their contactless debit cards at grocery stores, pharmacies, and more for added security and protection.

Credit: Comperemedia Direct

Capital One positioned its contactless capabilities as an extra layer of security and a way to not worry about carrying cash.

Credit: Comperemedia Direct

Comperemedia, a Mintel company, is an industry-leading competitive marketing intelligence agency. To find out more about Comperemedia’s products and services, please get in touch.